Financial literacy is one of those K-12 topics that’s hot right now. Under pressure from activists and policymakers, more states are requiring financial training for students. But does that training pay dividends for young people later on in their lives?

A new study provides some persuasive evidence that it does, if states pay attention to the nitty-gritty details of financial-literacy requirements.

The recent push for boosting students’ monetary savvy is highlighted in the work of groups like the Center for Financial Literacy at Champlain College, in Vermont, that routinely issue letter grades to the states on their financial-literacy policies. And it got a boost after the subprime credit disaster in 2008 led to the Great Recession and lots of handwringing about what young people know about borrowing and credit.

The new research, conducted by a quartet of economic researchers, found that young people in three states with graduation mandates for financial literacy tended to have higher credit scores compared to those in states without such requirements. They were also less likely to have accounts that were 30 or 90 days behind on payments, according to the study, which has been accepted for publication in the peer-reviewed Economics of Education Review.

It’s an important addition to the financial literacy conversation, because so far, much of the research on the effects of such policies has been mixed and marked by methodological flaws.

Previous studies have tended to measure outcomes in terms of knowledge, measured by post-course tests, rather than whether students’ actual financial skills or habits changed as a result.

Many of the former studies looked at outcomes right after the policy was passed, even though it often takes years for new policies to be implemented (think of how long it takes textbooks and teacher training to catch up).

“The big takeaway here is we need to stop saying financial education works or doesn’t work. We need to ask what kind of education works, for whom,” said Carly Urban, an associate professor of economics at Montana State University in Bozeman, who co-led the study.

Matching States

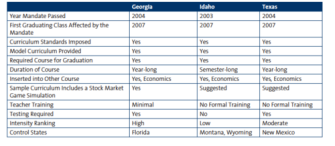

Urban and her three colleagues on the research team first spent time trying to get a grasp on what states have actually required for financial literacy since 2000. They found that 11 states had the most rigorous policies, requiring personal finance content to be completed before high school graduation. (Other states did not make the class a graduation requirement or left it to districts to implement.)

From these states, the researchers chose states whose mandates were in place long enough to produce results. They eliminated states that had multiple education reforms going on at the same time, such as changes to math curricula, that might have affected the results. And they chose not to include Louisiana, which experienced Hurricane Katrina in 2005, the same year it approved its financial literacy requirements.

That left Idaho, Georgia, and Texas. All three enacted new financial literacy requirements in the early 2000s, which kicked in for the graduating class of 2007. Here’s a look at what each requires (this comes from a brief summarizing the research):

To measure the effects of their policies, the researchers tapped the Federal Reserve Bank of New York/Equifax Consumer Credit Panel, which is a random sample of 5 percent of the credit report data from the Equifax credit bureau. From this, they selected records for 18- to 21-year-olds, from 2000 through 2014, looking at each in four-year increments to line up with each subsequent cohort of high school graduates.

To measure whether these state policies affected credit outcomes, the study uses a “difference in difference” methodology. Here’s how that works: For the young people in each state, the researchers generated a synthetic comparison group from individuals from other states, weighing things like state gross domestic product, unemployment rate, poverty rate, and housing prices to create a well-matched control group. Then they compared the financial outcomes for young people in each of these states, before and after the new mandate took effect, to its matched comparison group.

The size of the effects differed across states—an indication of how challenging it is to determine an average effect across different states and populations. It also highlights the differences in implementation. But there were some clear patterns.

The effects were most consistent for Georgia. Notably, the effects got stronger over time, probably as teachers became more familiar with the new financial literacy curriculum. By the third cohort of high school graduates after the policy took effect, young people’s delinquencies of 30 days declined by nearly 2 percent. Those over 90 days fell by 4 percent. And their credit scores rose by an estimated 27 points.

Effects in Texas were generally positive, too, with credit scores improving by 23 points for the third cohort of graduates after the policy was implemented, along with single-digit reductions in delinquencies.

In Idaho, effects showed up less consistently, but they did show significantly fewer delinquencies past 90 days for the third cohort of graduates. Credit scores in Idaho didn’t change significantly, although one reason for that might be because credit scores were far higher to start off with in Idaho than in the other two states.

For what often amounts to a fairly limited amount of class time, the financial-education policies do seem to give kids a head start on getting a secure financial footing, Urban said.

“I think what people are really interested in now, and they should be, is starting people off so their finances aren’t messed up by the time they’re 30,” she said. “This is one way to send the message that little things, like on-time payments and how to make a budget are important, and can actually go a long way to get people to a stage where they’re 30 and not in trouble.”

Related stories: